Refinancing to a 15-Year Mortgage: Is the Savings Worth It?

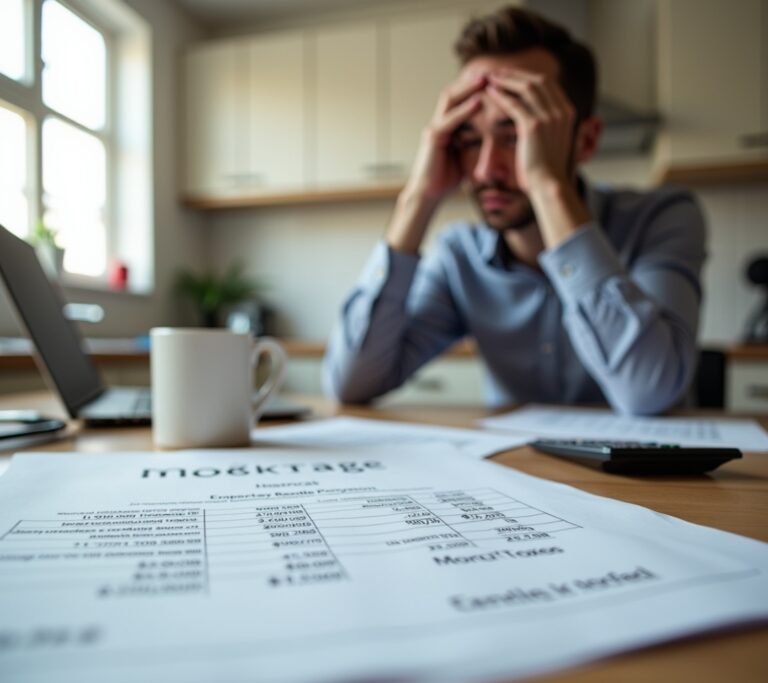

Switching to a 15-year mortgage saves a massive amount in interest — but your monthly payment jumps. Here's how to run the numbers for your specific loan.

Switching to a 15-year mortgage saves a massive amount in interest — but your monthly payment jumps. Here's how to run the numbers for your specific loan.

Refinancing on a fixed income comes with unique risks — from income verification challenges to resetting a loan you're close to paying off. Here's the full picture.

Refinancing a rental is trickier than a primary home — rates are higher and rules differ. Here's when it pencils out and what lenders require.

Property taxes are rolled into most mortgage payments via escrow — and when they rise, your payment rises too. Here's how it works and how to plan for increases.

Personal loans are unsecured and faster to get; home equity loans are cheaper but put your house at risk. Here's how to decide which fits your situation.

Once your HELOC enters repayment, payments jump significantly. These strategies — from refinancing to aggressive paydown — help you get out faster and cheaper.

Most refinances close in 30–45 days, but delays happen. Here's a week-by-week breakdown of what happens — and how to keep your refi on track.

Lenders require title insurance — and owner's title is optional but worth considering. Here's what each covers, what it costs, and when it's paid for just once.

Lenders require homeowners insurance as a condition of your mortgage — but coverage requirements vary. Here's the minimum they expect and how to avoid being underinsured.