USDA Loan Requirements: What You Actually Need to Know Before Applying

Advertisements

Here’s a stat that blew my mind when I first heard it — nearly 97% of the U.S. land mass is eligible for USDA loans. I remember sitting in my kitchen a few years back, convinced I’d never qualify for one because I didn’t live on a farm. Turns out, I was dead wrong! USDA loan requirements are way more accessible than most people think, and honestly, understanding them could save you thousands of dollars on your next home purchase.

What Exactly Is a USDA Loan?

A USDA loan is a government-backed mortgage offered through the U.S. Department of Agriculture. It’s designed to help low-to-moderate income borrowers buy homes in eligible rural and suburban areas. The biggest perk? No down payment required — which is kind of a huge deal if you ask me.

I actually stumbled onto USDA loans when a buddy of mine bought a house just 20 minutes outside of Nashville. I was like, “Wait, that’s considered rural?” Apparently yes, and he got a zero down payment mortgage because of it. It completely changed how I thought about homebuying options.

Income Requirements — This Is Where It Gets Tricky

So here’s the thing. USDA loans have income limits, meaning you can’t make too much money to qualify. The household income cap is typically 115% of the area median income, but it varies depending on your location and family size.

You can check the USDA income eligibility tool to see if you fall within the limits. One mistake I see people make all the time is they only count the primary borrower’s income. Nope — USDA looks at the income of everyone in the household, including adult children living at home. That caught a friend of mine off guard and almost derailed her application.

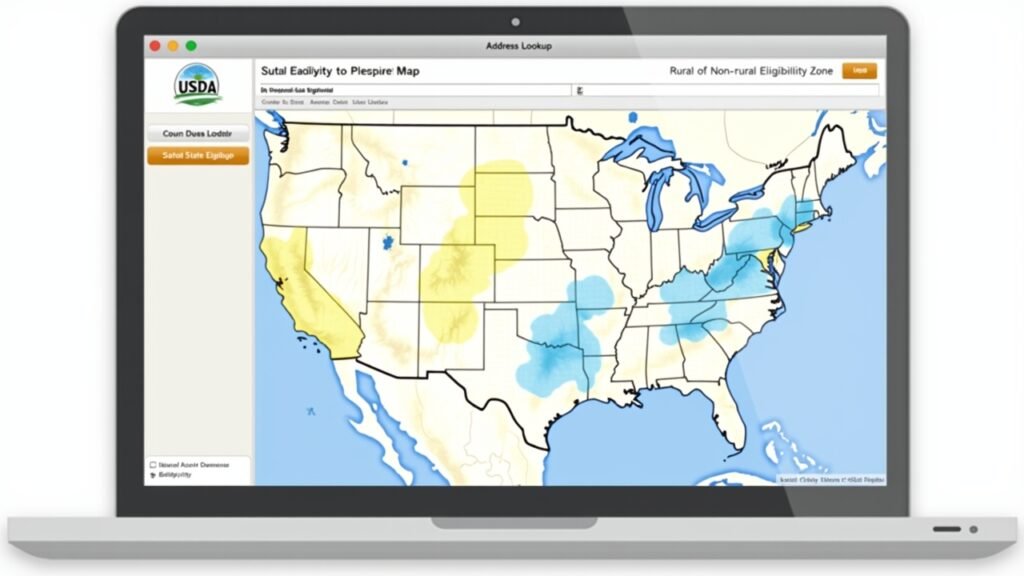

Property Eligibility — Location Matters More Than You Think

Not every home qualifies. The property has to be located in a USDA-eligible area, and it needs to be your primary residence. No investment properties or vacation homes allowed here.

The USDA property eligibility map is honestly your best friend during this process. Just plug in the address and it’ll tell you right away. I’ve seen homes literally one street apart where one qualifies and the other doesn’t — it’s wild. Also, the home has to meet certain safety and livability standards, so a fixer-upper that’s falling apart probably won’t pass the appraisal.

Credit Score and Debt-to-Income Ratio

Now let’s talk numbers. Most lenders want a minimum credit score of around 640 for a USDA loan, though technically the USDA itself doesn’t set a hard minimum. If your score is below 640, you might still get approved, but expect a lot more paperwork and scrutiny.

Your debt-to-income ratio matters too. Generally, lenders look for a DTI of 41% or lower. That means your total monthly debts — including the new mortgage payment — shouldn’t exceed 41% of your gross monthly income. I’ll be honest, I was right on the edge of that threshold when I was exploring this option, and it was stressful. Paying off a small credit card balance before applying made all the difference.

Mortgage Insurance — Yes, There’s a Catch

Even though there’s no down payment, USDA loans do come with mortgage insurance. There’s an upfront guarantee fee of 1% of the loan amount and an annual fee of 0.35% that gets rolled into your monthly payment. Compared to FHA loans though, these fees are significantly lower.

Think of it this way — on a $200,000 loan, you’re looking at about $58 per month for the annual fee. Not nothing, but honestly pretty manageable when you consider you didn’t have to scrape together a down payment.

Your Next Move Starts Here

Look, USDA loans aren’t for everyone, but they’re an incredible option that way too many people overlook. The zero down payment feature alone makes them worth investigating, especially if you’re buying in a suburban or rural area. Just make sure you check your income eligibility, verify the property location, and get your credit score in decent shape before applying.

Everyone’s financial situation is different, so take this info and tailor it to your own circumstances. And if you’re hungry for more mortgage tips and homebuying guidance, head over to the Mortgage Margin blog — we’ve got tons of posts that break down the confusing stuff into plain English. Your dream home might be closer than you think!

Advertisements